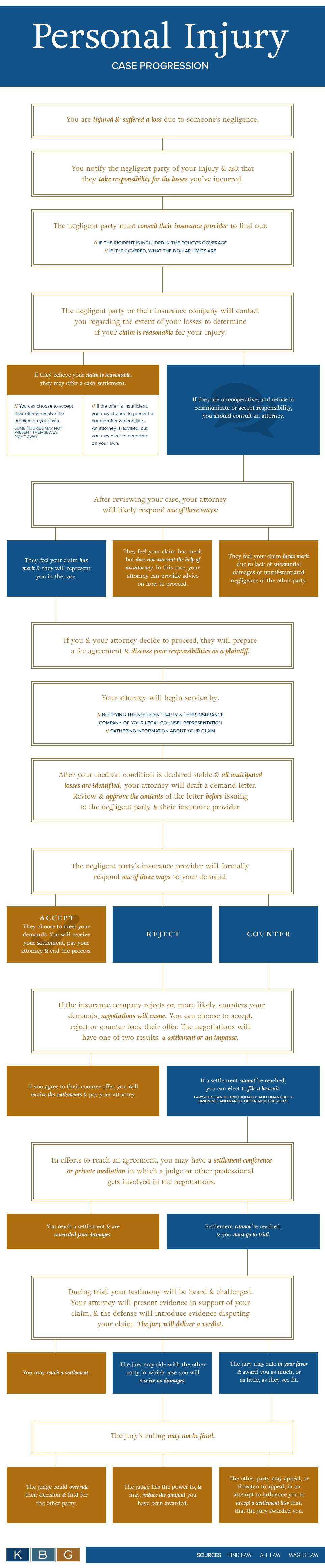

How a Personal Injury Case Progresses

“Today is the day I’m going to slip and fall,” said no one ever. Accidents happen all the time. The “slip and fall” category alone results in over 8 million trips to the hospital ER. What happens if you’re the victim of this type of accident? If it occurs around your home, you would be responsible. However, if the accident happens at your workplace or a business, it might not be your fault. If the accident resulted in a severe enough injury, you might be entitled to financial remuneration. To get there, you’ll need to follow a particular course of action.

This work is licensed under a Creative Commons Attribution-NoDerivs 3.0 United States License.

Step 1: Notification

Ascribing negligence doesn’t automatically translate into a payment, but it is the first important step in a personal law injury case. Although you might not be thinking about blame in the immediate aftermath of an accident, it is important you notify the business or worksite manager right after the accident. You need to go on record that an accident just occurred at that place in that moment. It won’t help to fall and then come back days later to make a claim without proof.

Step 2: Contacting Insurance Companies

The negligent party is what the lawyers will call the defendant in your lawsuit. This is the owner of the business where the accident took place. Once that negligent party has been notified that an accident took place, they will be contacting their insurance company. At that point, representatives from the insurance company will take up the case and open communications with you. They will want to know the extent of your injuries and any associated costs. They will also conduct their own examination to determine the level of negligence on behalf of their client.

Step 3: A Possible First Settlement Offer

If the insurance company determines your claim is reasonable, they might offer a quick settlement. You are well within your rights to accept that settlement, but that would end the case. You couldn’t go back months later with more physical therapy bills and expect to get reimbursed.

This is probably the best time to contact an experienced attorney who handles personal injury matters. They would be in the best position to determine if the settlement offer is fair and whether you should accept it.

Step 4: Rejection of Your Claim

An insurance company is well within their rights to reject your claim. In fact, they will most likely do that as a matter of function. If a personal injury attorney feels your case has merit, they can proceed with a lawsuit. That will mean notifying the negligent party and their insurance company that essentially you’re not going away without a fight.

Step 5: Evaluating Your Condition

It is difficult to sue a business for an accident until your medical condition stabilizes. You simply can’t put a price on your treatment until it is over. That is not to say you can’t be compensated for future bills or pain — it just has to be established first. Once your attorney has assessed the totality of your physical condition, they will generate a demand letter.

Step 6: Second Possible Settlement Offer

Upon receipt of the demand letter, the insurance company has three options: accept, reject or counter. Accepting the offer means they’ll be cutting a check for the demanded amount, and the case will be closed. Countering will have them presenting with an amount that is lower. A rejection signifies they’re digging in their heels and aren’t ready to make a payout.

Step 7: Proceeding to Trial

There could be a few rounds of counter proposals. If an agreement can’t be reached, your lawyer will proceed with the lawsuit. This will require a series of depositions and evidence gathering. Both sides in this matter will have access to all that evidence. You will probably also be deposed by their attorneys.

Before the trial begins, there might be another settlement offer. This usually happens when the insurance company recognizes your resolve.

Step 8: The Trial

If the insurance company still resists, the trial will proceed. Both sides will have an opportunity to make their case in front of a jury. That jury can render an award amount in your favor that could be rejected or reduced by the judge. If the insurance company loses, they have the right to appeal. That means you won’t be seeing any money until the matter is finally solved. This is another way for an insurance company to attempt to make one more low settlement offer.

It is easy to see how important it is to have qualified legal counsel through every step of this process. The best decision you can make is an informed one. Contact KBG Injury, your go-to law firm for personal injury cases.

The personal injury attorneys at KBG Injury Law are all experienced litigators. Almost all of them represented insurance companies prior to becoming advocates for injured people, which provides them with a unique perspective and insight into how these companies operate. They also offer extensive courtroom experience if going to trial is the best legal alternative for the client.

[Read More]